53

magazine

ALRAQABA

some expenses as assets.

- Manipulation of sold cost assessment pol-

icy.

- Non-reconciliation of the provided reve-

nues.

2- Manipulation of some expenditures, as well

as to their carrying over to another later or

early periods or transferring expenses based

on personal assessment of current account-

ing period.

3- Inflate some accounts e.g. profits, current

assets and equity through concealing the ac-

counts receivable and bad accounts.

4- Inflate the sales and profits through sales

inclusion of unconfirmed sales contracts.

5- Manipulation of the inventory turnover

though unusual inventory reduction.

6- Innovative Accounting can be used to sup-

port and strengthen the financial position. This

could be done through the utilization of vari-

ous methods such as: delaying the suppliers

due payments and attaining credit facilities, as

well as to collecting advance /down-payments

from customers.

Factors that would enable the creation, and

increase the use of innovative accounting are

shown in the following diagram:

II: Innovative Accounting & Work Quality

Due to the importance of audit quality, the In-

ternational Federation of Accountants issued

the Audit Quality Framework, since innova-

tive accounting starts threatening the quality

of the work, as it affects the decisions and

reports. The Quality Framework explains the

significance of creating a work friendly envi-

ronment that would restrict the use of inno-

vative accounting methods, despite the lack

of a defined mechanism to assure the quality

of the audit work in accordance to the Quality

Framework.

Quality Audit contributes in detecting innova-

tive accounting, restricting its utilization and

enhancing the quality of the supervisory out-

puts. Therefore, the International Federation

of Accountants encourages auditors to con-

duct quality audits in a continuous manner

b y

the use of the quality framework. In

order to enable auditors of per-

forming the quality audits to

detect innovative accounting

methods, a proper work envi-

ronment shall be established.

The said environment would en-

able the application of the quality framework

on various institutions regardless of their size

and work nature.

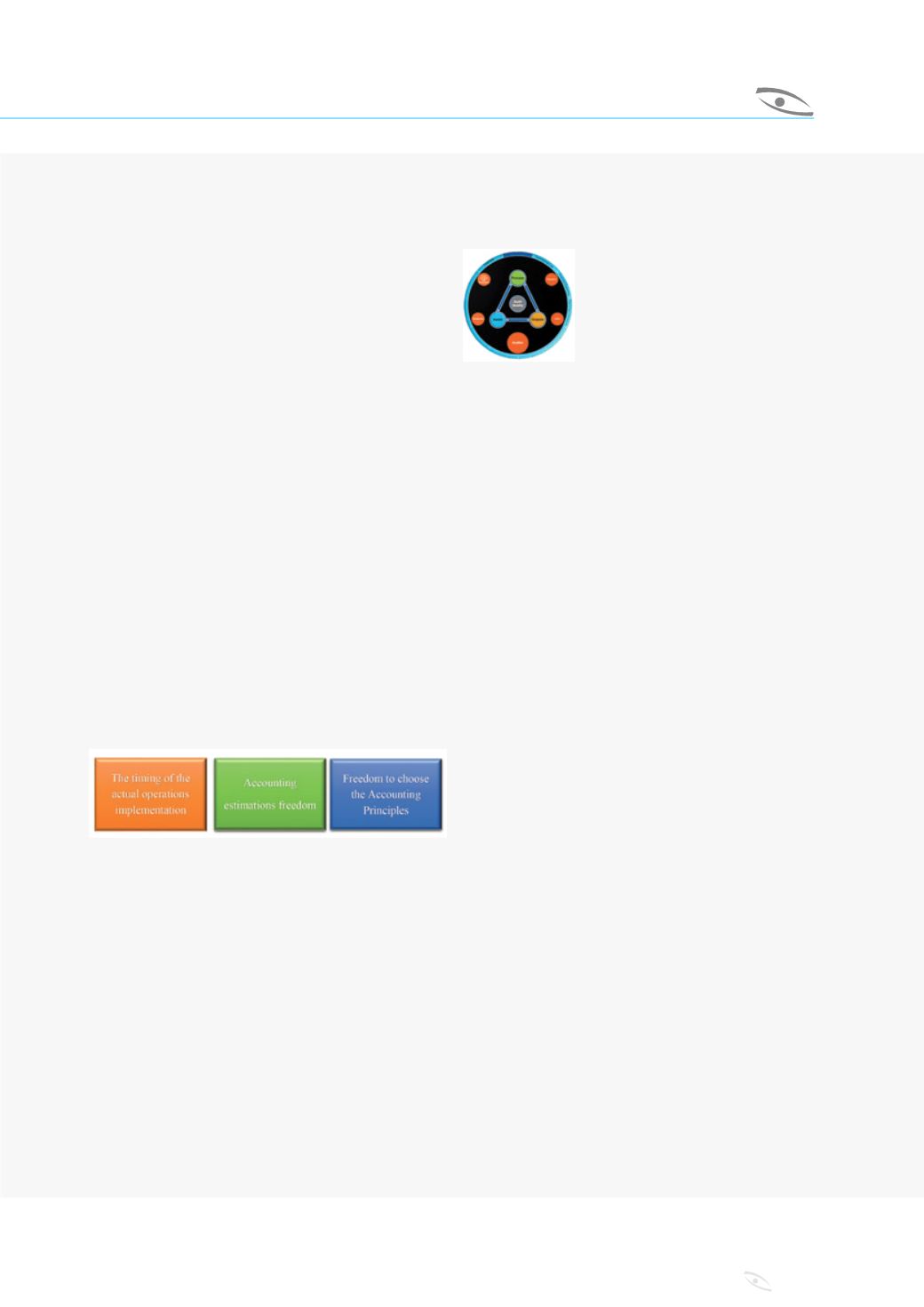

The Audit Quality Framework

Key elements of the Audit Quality Frame-

work:

Inputs:

Auditors are the key element and

are largely relied on; therefore, they must be

persons of high professional ethics, great ef-

ficiency and experience alongside with pos-

sessing the sufficient information that would

enable them of performing the assigned tasks

and having a knowledge of the innovative ac-

counting methods.

Processes:

Audit quality obliges the auditor to

perform extensive reviews, as well as to ad-

here to certain standards and laws that would

enable the detection of several cases of inno-

vative accounting utilization.

Outputs:

outputs includes reports and the de-

tection of fraud cases by the assigned audi-

tors.

III: Innovative Accounting and the Audit Pro-

fession

Auditing is a key factor in eliminating the in-

novative accounting phenomenon, as it helps

in reducing the misunderstanding between

the top management and the investors. On

the other hand, auditing relies on the auditor’s

abilities and capabilities to detect cases of

fraud and manipulation, as well as to restrict

the innovative accounting methods. Many

studies have proven that the audit profession

is closely related to detecting cases of inno-

vative accounting, however the auditor`s “ef-

ficiency” is the most significant factor in de-

tecting the said cases. The auditor`s abilities

greatly relies on the experiences, acquired