48

magazine

ALRAQABA

Issue Research

5- Audit quality concept approved by the 9th

session of the Arab Organization of Supreme

Audit Institutions.

Systems and methods of audit quality

The world came across of the financial markets

liberation, whereas in the financial crises of 2008

that threatened many institutions, different ques-

tions occurred about basic matters relating to the

nature, scope of, and communication methods of

the review process although the accounts audi-

tors were not considered responsible. Commonly,

review reports preciseness is considered one of

the review quality signs. The accountant auditor’s

report may affect positively the audit quality and

the review process development. Therefore, we

should focus on the most important sides that

leads in return to improve and develop the audit

quality.

1- Audit Report Development.

2- Accounts Auditor Independency.

3- Audit process transparency enhancement.

1- Development of audit report

The report is considered the final product of the

audit process which represents the guideline for

the audited financial statements users, therefore,

it is quite important for this report to be clear ,con-

cise, and compatible with the professional stan-

dards that governs the preparation of this report

which are financial statements presentation. The

report should include whether the financial state-

ments are prepared according to the common

accounting principles.

2- Independency of the Accounts Auditor

Real independence is the opinion or intellectual

honesty of the accounts auditor, and the fact that

he should not follow anybody in any way, and is

not subject to the client impact in his decisions

taking. There is also the standard of professional

care exertion while practicing the audit process in

a professional sufficient manner. The independen-

cy of the auditor is considered vital and important

for the audit quality. One of the suggestions for

the auditor’s independency enhancement is his

obligatory periodical change, the supporters of

this proposal view that it improves the latter inde-

pendency, and thus the review process. Whereas

the new auditor shall review the work of former,

prohibit the audit team from having relation with

the company management subject to their audit.

Moreover, the obligatory change of the comptrol-

ler shall limit the development of the relation be-

tween the auditor and the client that decreases

the auditor independency and objectiveness.

Long term contracting with the auditor may lead

to decrease the level of the audit quality and the

auditor’s work efficiency that becomes lower by

time.

3- Enhance transparency of the audit process.

(PCAOB ) suggested to disclose the auditor who

performed the audit process. Other disclosures

relating to the first part is disclosure of the auditor

name which shall increase the personal feeling of

responsibility, it provides useful information for in-

vestors, encourages the auditor to pay attention,

supports transparency, improves interaction, and

facilitates the accountability of the auditor when

failure occurs, and also encourages his indepen-

dency.

Audit Quality International Standards

Audit quality standards applies on all sizes of

economical and administrational units’ in both of

the private and public sector that are working in

various fields. Before discussing the audit quality

framework issued by the International Standard

Council, the audit quality contents may be sum-

marized as follows:

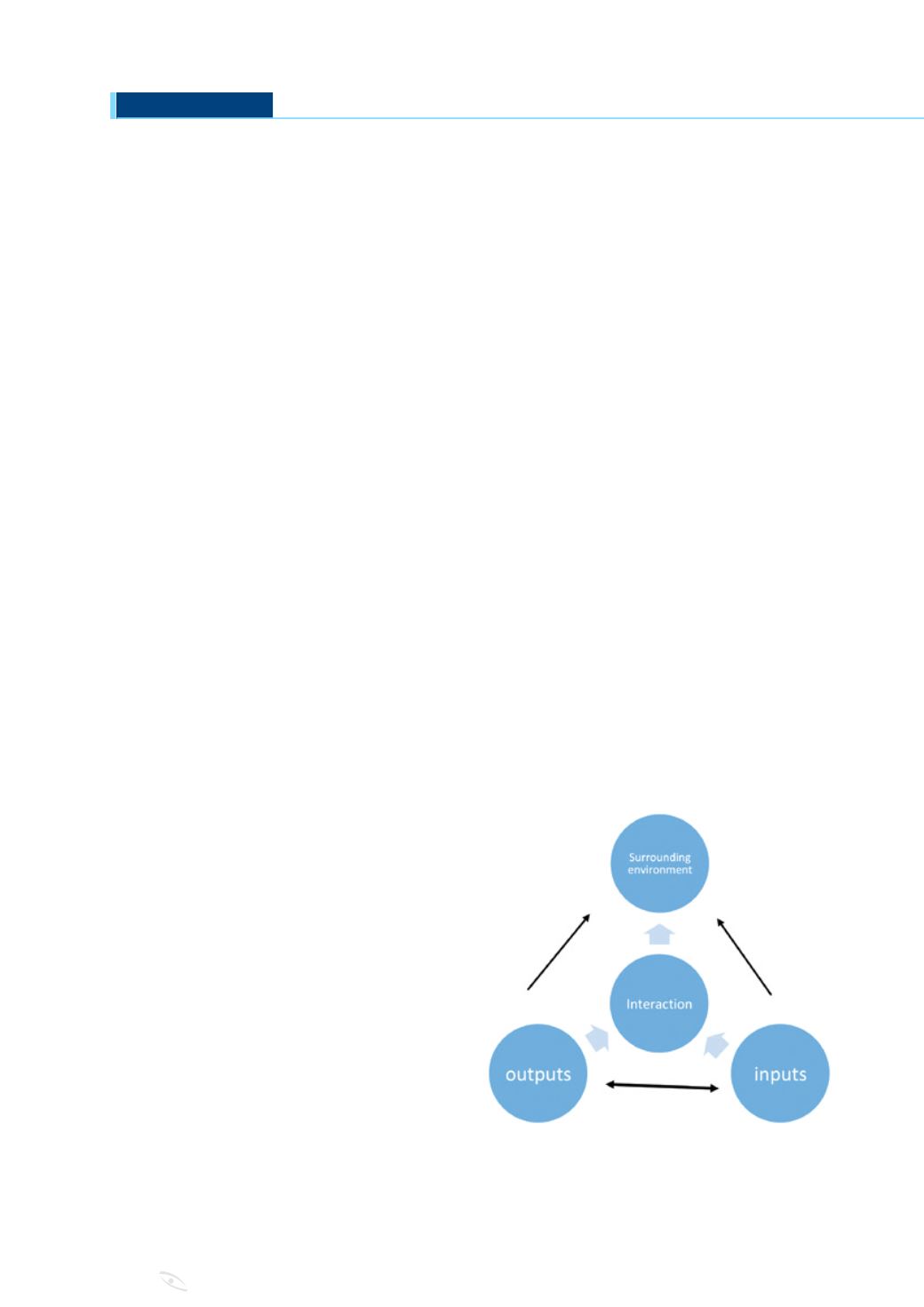

The elements of the audit quality consist of the

audit environment, inputs, outputs, and the inter-

action that goes between them, and then the in-